Things are about to get very interesting

The simple solution to an anticipated recession.

After I wrote about money, inflation and poverty, some readers contacted me privately arguing that I’d got it wrong. In essence they advanced the Friedman doctrine about controlling the money supply through interest rate manipulation as the proven key to managing inflation. Meanwhile, I’m reading plenty of reports warning of an oncoming recession.

Both gave me pause for thought but left me head scratching. My memories of interest rate ups and downs reminded me of how that combined with reduced public spending left many people worse off but that some won out. Why did that happen?

It turns out that the measure of inflation used to dictate policy in this regard is incomplete because it doesn’t reflect the real world. Every consumer understands this. For example while the headline rate of inflation is 7% and expected to reach 10% by autumn, we already know that the forthcoming energy price cap review will likely lead to cost increases of 40%. How can we explain this disparity?

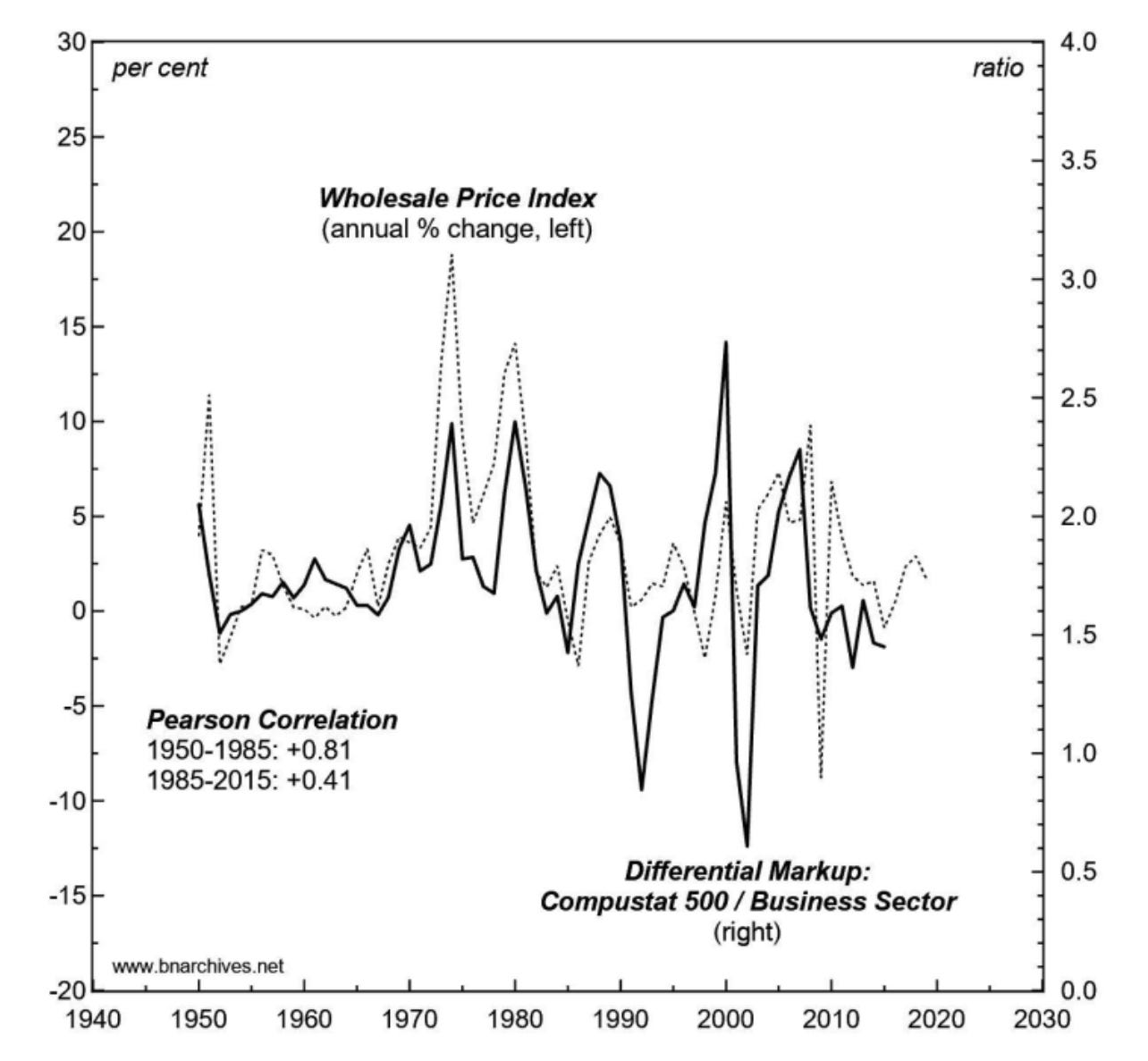

In November 2021, Blair Fix laid it out in a long read titled: The Truth About Inflation: Why Milton Friedman Was Wrong, Again. In that paper, Fix demonstrates two things:

How average inflation as a measure tells us little about its cause and misdirects us about the variability of prices within the basket used to measure inflation.

That individual price control is in the hands of oligopolies and so tends to benefit large businesses.

It is an illustration of that second contention I use as the image at the top of this story.

Fix proves the first contention by plotting commodity price variation against the commonly understood average over time. His second contention is supported by a similar analysis that looked at who gains during inflationary periods. Fix acknowledged that his analysis has problems for creating theory but equally, he argues that monetarism, based as it is on Friedman’s theorising is fundamentally flawed because while Friedman works in theory it only partially explains what we see in the real world and is tied to a way of thinking that makes the wrong assumptions.

A growing number of people are pointing out that during the COVID pandemic, some firms made out like bandits and that generally, those with wealth (and assets) did well. Prof Scott Galloway for example, regularly talks about how the American middle class has been hollowed out while the top 1% have disproportionately gained when measured over the last 40-some years and especially in the last few years. (Check out his newsletter and podcasts for much more on this topic)

Now we see energy companies making out like bandits. And when it comes to market control, in a a past life: I often said ‘never bet against SAP’. Why? Because they are deeply embedded in a large percentage of the world’s companies and, according to many contemporaries, cannot be replaced - not any time soon. That’s one of a few reasons why SAP often appears like it is defying gravity - at least at the financial level. It is that market control that allows it to set prices it chooses to satisfy its economic goals. And that’s despite naysayers forecasting doom for SAP from time to time.

Now, I know that nothing is forever. We can see that clearly in the push to replace fossil fuels with renewables. But who will benefit? I’ll stick my neck out here and say it’ll be the same band of suspects we know about today. But I digress - slightly.

So if you buy the ideas that Fix explains, then it follows that governments cannot, of themselves, control inflation. But they can (and do) put forward control policies based on their ideological position.

That’s why today, you see a government that has reverted to what amounts to austerity measures as a means to ‘control’ inflation. Who benefits? Those who hold assets. Right now I’m delighted that I can get 10x the interest rate I was getting a year ago but that’s because I have savings. What about my neighbour who doesn’t and holds down a relatively low income job but who is faced with the same price hikes for energy that I face? Worse still, what about those who are at the bottom of the social ladder?

The situation is now so critical that it is spawning some novel ideas. I read for instance that the CEO of Scottish Power is saying the government should cut the fuel bill of 10 million people in need by £1,000 to help alleviate a coming ‘fuel or food’ crisis. Sounds like a good start but then he adds that the cost could be repaid by slapping every energy user with an annual £40 charge over the coming decades. Not. Going. To. Fly.

In the meantime, we have an ongoing war, the effects of which are felt in a wide variety of consumer and business costs, especially in Europe, but rippling around the world. That won’t end anytime soon. And if pundits are right then we’re staring down the barrel of a recession that will only inflict more misery on an already impoverished nation. If a recession comes along then government faces a choice. It either spends as it did during the pandemic to support the most vulnerable. Or, it sits on its hands. The latter looks increasingly likely.

To me what’s glaringly obvious is that those who are in opposition to our current government are not articulating alternative policies with the benefit of explaining why their measures make better sense. It is all very well their leader berating the government for having ‘run out of ideas.’ But the measures proposed - a windfall tax on energy companies being the headline we all hear - does little to solve for the systemic problems that monetarism brings with it. It comes back to Fix’s argument for the ideological roots of managing inflation.

If you agree that the impact of variability in components of inflation and the ability of powerful entities to manage their own wealth are at the heart of economic and social problems then it is a short step to developing policies that tackle those issues. But that brings with it a prospect recent governments have sought to avoid. It means taking on powerful entities in a concerted fashion as much of the world has done in Ukraine in thwarting a powerful threat in Putin’s Russia. Who’s up for that?