The new abnormal - an opportunity at risk of loss

The lack of innovation in thinking is stifling the prospect of step change in a post pandemic, war torn time.

I’ve been quiet for a fortnight as I’ve wrestled with understanding how pandemic induced opportunity has largely been lost and looks set to be lost again even while there’s a war impacting us all.

In my view, the COVID pandemic presented a unique opportunity to reset what it means to work in a largely services based economy. I hoped we’d see the emergence of a more caring and supportive work environment. Looking back, that opportunity seems lost as swathes of people snarl up our roads returning to places of work.

I get that there are arguments to continue WFH, so-called hybrid work and situations where people have to be in a place of work. Even so, much of what might have been achieved has ebbed away as businesses return to the command and control Marxist theory of labour.

During the pandemic I saw plenty of potential for broad based innovation but the fundamentals went untouched. In the year up to my retiring and the first year of pandemic regulation, innovation stalled, incrementalism flourished.

A year later and nothing much changed except that the fragility of global supply chains became glaringly apparent. As a parochial example, it took four months for me to receive an item that normally takes two weeks and six months to receive an item ostensibly built in Europe but dependent upon parts sourced in China. Go figure.

No sooner had we seemingly overcome the worst elements of pandemic disruption and war broke out in Ukraine, triggering an energy cost crisis that has no immediately obvious end in sight and which impacts the cost of everything.

Layer in the utter shambles that is Brexit and the U.K. faces this year’s prospect of having the lowest GDP growth among the G7. The most recent figures also show that insolvencies spiked in the year to March 2022 by 111%. And all the while we see millions falling into real poverty while the wealth inequality gap continues to grow.

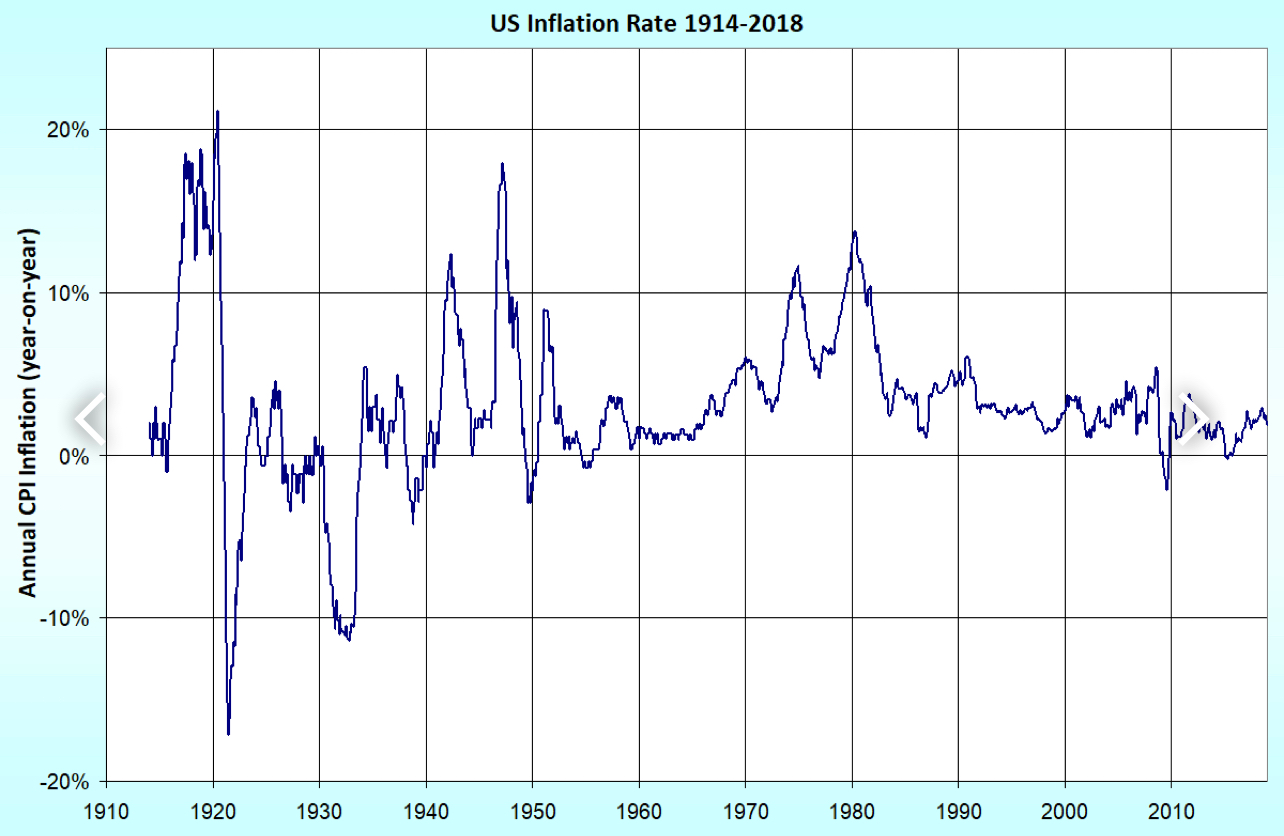

Our government’s answers are little short of idiotic let alone illogical. How is it for example that ‘we’ found billions to ‘pay’ for a raft of COVID related reliefs yet cannot find the money to help the most vulnerable at a time when cost inflation is at a reported 7% and climbing, largely due to the fuel crisis?

How can we throw many millions in aid to the Ukrainian war effort without any obvious obligation to repay yet plan making repayable loans to British households in an effort to temporarily soften the blow of energy price rises coming later in the year?

This crisis is presented as temporary in the same way that COVID is/was temporary. So how is it that government finds money for one thing and not another?

According to the Chancellor, today’s problem is about the risk of fueling inflation. That makes no sense. If government can find direct grants by printing money as it did during the pandemic without fuelling inflation then why not now? After all, successive governments have printed money at will since the late 18th century. We call it the National Debt.

Government likes to scare us by saying that Debt stands at a whopping £2 trillion but if political economists like professor Richard Murphy are correct, and I believe he is, then that number is overstated by at least £800 billion. (Check his chapter on debt.) And to those who worry about the cost of servicing the debt I say this - how is it that people like you and me plus all the commercial banks have no problem saving or buying government bonds which carry interest?

The arguments put forward by our government are rooted in a failed theory of economics supported by a failed ideology of low taxes (duh - when we’re seeing the highest rate of taxes on individuals in 70 years) coupled to the notion of a small State. In some circles this set of ideas is wrapped up in a Back to Basics (Tory) view of the world.

The last time we saw that idea was during the time of John Major’s government. Ironically, it was also a time that preceded the exposure of rampant political sleaze, just as it has done recently. The difference is that Major is widely regarded as a decent politician and prime minister. By comparison, Boris Johnson is, by any measure, a charismatic clown, chancer and serial liar who has surrounded himself with what look like intellectually challenged ministers. Smart people surround themselves with smarter people. Johnson has gone the other way, appointing a series of media punks who don’t understand shit from shinola.

Rishi Sunak, the Chancellor, is the exception except that he comes from the world of hedge funds and Goldman Sachs. It is they who cling to the old economic order. Why? Inflation is the stated menace coupled to a claim that business investment will stall if inflation takes off. In short, it’s all about what Sunak thinks is best for business first.

The investment claim might be well founded in some sectors that are already stressed such as hospitality. But since the current inflation spike is largely attributed to what is thought to be a temporary problem then why would sensible leaders who think for the long haul materially change their plans? Especially in energy which is an industry requiring long term investment. Indeed, the head of BP, the UK’s largest energy company recently said that inflation makes zero difference to the company’s investment plans. Hardly surprising when you know that U.K. energy companies benefit hugely from investment subsidies.

All of which led me to call up Murphy. His solution, which is regularly sought after in mass media, is easy to understand and makes sense.

The U.K. government operates a monetary system that allows them to print money at will. They’ve done that at various times so why not now?

The notion of a National Debt is overblown. We’ve run ‘debt’ for hundreds of years without issue.

The fear of ‘tax and spend’ with which Tories demonise their main opposition is wrong headed. All governments spend and then tax.

Since the U.K. offers tax incentives to save which have consistently proven popular then why not create a new incentive tied to green investments that also pay an enhanced rate? Better still, use the existing system of incentives to mandate qualification based on green investing?

Overhaul the tax system so that the myriad of allowances, exemptions and incentives that only benefit the most wealthy are largely removed or at least pared back substantially.

There is more but that’s the bones of what he suggests. And he’s not alone.

On its face, Murphy’s solution reaches well beyond helping the poorest in our society. That’s as it should be because what is needed are practical long terms solutions that can also accommodate short term shocks. What’s not needed are ideologically driven policies that avoid addressing past and repeated economic failings.

The problem is that none of the mainstream political parties understand these arguments. Worse still, the public trust in politicians is abysmally low. For evidence you only have to look at how the recent National Insurance increases are regarded as a tax grab in the popular press while they have been positioned as a way of paying the NHS need for expanded funding. Paradoxically, past surveys have consistently said that the public would support a tax increase of this kind yet here we are.

The real problem then is that the public cannot see and does not believe that government is acting in our collective best interests. This contrasts sharply with countries like Denmark where taxes are relatively high but the standard of living is good and education at university for example is free. In Denmark, they see their tax money at work for the public good. Murphy’s green investment agenda achieves the same thing while operating a fairer tax system allows for the kind of social support needed by millions of British people.

Nothing is that simple but after one missed opportunity for innovative thinking surely now is the time to reset. Again.

We rarely get two bites of the cherry and when we do it’s even rarer for those opportunities to come one after another. It is within our grasp if our politicians can think with an innovative and radical mindset. Where are these people?

Your government should not hope that new trade agreements with newly developing countries like India can replace the EU, give a boost to your economy or that a new open innovation visa model will give a flip up to innovation and growth.

As far as the basic issue goes, it is fairly simple. A lot of so called growth and innovation in recent years was simply the behavior of crowds with too much money. The business world is now feeling the tightening and the self defined checks/balances are kicking in, btw they should have controlled this much earlier.

How do you print money and (lend more to) spend more, when inflation is soaring, when supply chain is choking and when the bankers are increasing rates? Consumers are hurting and the wage inflation cannot match?

Before a new cycle of sensible and logical innovation and growth begins, the existing must fizzle out. And the money supply must tighten. Public spending is either a solution for efficient Demark or for the in-efficient trickle down poor/developing world.

Not for the UK.

On oil/gas prices, I saw an interesting video earlier today explaining that the price raises are here to stay: https://www.youtube.com/watch?v=AQbmpecxS2w - "Why Gas Got So Expensive (It’s Not the War)"