BNPL - the new way to keep vulnerable people poor.

BNPL - the new way to keep vulnerable people poor.

Buy Now Pay Later (BNPL) is the latest in tech driven finance as a tool to part you from your money. Beware.

BNPL is emerging as the new hotness in the financial services market to the point where valuations for firms operating this…how shall I call it…thinly disguised credit wheeze…are at insane levels. Check the graphic at the top, taken from the ProfG newsletter where he says:

By most measures, BNPL services aren’t even good credit offerings. With a traditional credit card, you pay nothing up front, then you’ve got, on average, five weeks to pay without incurring any fees or interest. Closer to two months if you manage your billing cycles carefully. Carrying a balance will cost you, though, 1%-2% in interest per month. Miss a payment, and you get a late fee, about $30 — on which you’ll also pay interest.

In the short term at least, BNPL terms are worse. Take Afterpay. When you buy your new jeans, you have to come up with 25% of the money at purchase, then the lender gives you six weeks to pay off the remainder, in three installments. Miss an installment, and Afterpay hits you with a late fee. Continue in arrears, and the late fees increase, up to a cap of 25% of the purchase price. Also, you need a debit or credit card to make payments to Afterpay. Other providers have different fee and interest structures, but the basic model is the same. It’s credit.

According to Galloway the attraction, especially to younger folk is that BNPL is not pitched as debt and firms in this space emphasise the fees they take from merchants which are way higher than the credit card companies. In this situation, it’s not hard to see why BNPL firms are attractive to investors. But for how long?

Yesterday I heard a news story the nut of which is that U.K. regulators are concerned about BNPL terms but regulating them will take time. WTAF?

To my simple mind, BNPL is nothing new (remember those TV ads that enticed you to buy furniture but defer payment for many months?) and smacks of the old hire purchase which was first regulated back in 1938. That was a time when those providing credit preyed on the vulnerable. In essence, the Hire Purchase Act was an effort to ensure that consumers were able to see how much they were paying and, crucially, the terms of payment.

At a stroke, the Act killed off the tally man, the person who knocked on your door each week to collect what you owed. Today, those collections happen electronically but as we are seeing, the hidden cost for those who default can be crippling. Over to Galloway again:

Australia’s financial regulator found 15% of BNPL users had to take out another loan to make their payments, and 1 in 5 had to cut down spending on essentials to make them. In 2019, Australian BNPL providers raked in $43 million in revenue from late fees, up 38% from the previous year. At a major U.K. bank, 10% of customers making BNPL payments overdrew their checking accounts in the same month. The authors of one study dubbed BNPL users “Generation Debt Trap.”

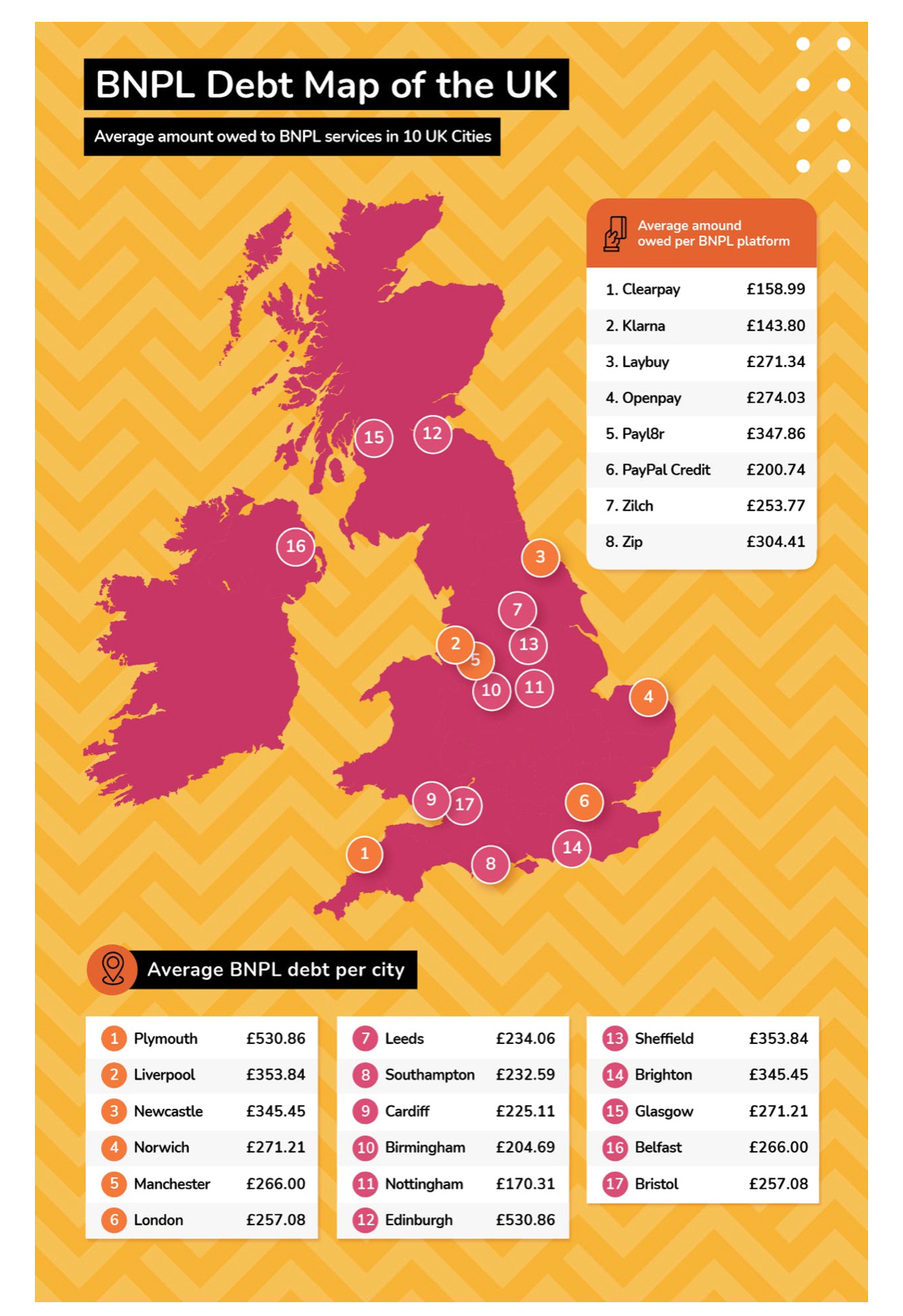

And if that wasn’t bad enough, guess where the U.K. BNPL hot spots are? Right where you’d expect them - among the more deprived regions of the country as this graphic illustrates:

I’ve long been a harsh critic of deceptive marketing and to me, BNPL is among the sleaziest I’ve seen. Tempting those who are most vulnerable is always despicable. What’s more despicable is the way in which regulators are dragging their feet at a time when consumers are stressed.

One answer is transactional transparency. It’s too easy to buy stuff you later regret or really don’t need. eCommerce platforms make it ridiculously easy to buy pretty much anything by the press of a button. Couple that with BNPL and you have a toxic mix in the making. Overlay that with what I term Black Buying Week and you can readily imagine a miserable future for those caught up by the allure of BNPL. It should therefore be no surprise that in 2021, the greatest concern among BNPL consumers is their mental health.

According to Galloway, TikTokers are hitting back. Nice - but not enough. Now is the time for strong regulation so that this latest attempt to ensure vulnerable people remain poor is killed off.

Sadly, I’m not holding my breath. The current U.K. government must qualify as among the most inept and corrupt in Parliamentary history. I’d be surprised if regulating BNPL is even close to the top of lawmaker agendas. However, if the media could, for once, get its shit together and kick up enough of a stink, then maybe, just maybe, this financial cancer can be killed off before it starts killing people.

In the meantime, recognise BNPL for what it is - high priced credit.

Excellent and important article. Along with the useless EU & UK regulators the current US president was instrumental in turning the state of Delaware into a legal credit card debt mill.

Career politicians are making it harder and harder for the people to have regulations that protect them from the undermining constantly scheming usury scum underclass.

https://www.motherjones.com/politics/2019/11/biden-bankruptcy-president/